Overview

Commercial real estate lending is a cornerstone of business finance that empowers owners and prospective investors to acquire, develop, and refinance income-producing properties. For property owners, understanding how to leverage CRE financing is essential to expanding your portfolio, optimizing returns, and planning future developments. This comprehensive guide is designed to provide you with the knowledge necessary to navigate the complexities of the lending process, ensuring that you make informed financial decisions that align with your investment strategy.

If you're interested in how property performance ties into financing decisions, be sure to check out our Cap Rate Formula: A Comprehensive Guide for deeper insights.

Understanding CRE Lending

Commercial real estate (CRE) lending differs from residential financing in scale, complexity, and risk assessment. For commercial property owners, tapping into CRE loans can unlock opportunities for portfolio expansion, property improvement, and business growth. Lenders evaluate not only your personal financial strength but also the property’s performance potential. This dual focus ensures that both the asset and the borrower are well-positioned to meet debt obligations.

As a property owner, it is important to understand how various lending options can be tailored to your business model. Whether you’re looking to acquire a new property, refinance an existing asset, or undertake a redevelopment project, knowing the nuances of CRE financing can help you secure terms that are both competitive and sustainable. For further reading on integrating effective property management with financing, explore our Property Management Software for Small Landlords guide.

Key Terms & Concepts

Before engaging with lenders, familiarize yourself with these fundamental terms and concepts:

- Loan-to-Value (LTV): This ratio compares the loan amount to the property’s appraised value. A lower LTV indicates less risk for the lender, and for owners, it often means better loan terms.

- Debt Service Coverage Ratio (DSCR): The DSCR measures the property’s ability to cover its debt obligations with its net operating income (NOI). A DSCR greater than 1.2 is typically required, ensuring there’s a cushion above the minimum needed to service the debt.

- Net Operating Income (NOI): NOI is calculated by subtracting operating expenses from the property’s gross income. This figure is critical for evaluating the property’s financial health and loan eligibility. For more details on how NOI influences property valuation, refer to our Cap Rate Formula: A Comprehensive Guide

- Amortization Period: This is the period over which the loan principal is repaid. A longer amortization period can lower monthly payments but may result in higher overall interest costs.

- Recourse vs. Non-recourse Loans: Recourse loans hold the borrower personally liable for the debt, whereas non-recourse loans limit the lender’s claim to the collateral property alone. Many property owners prefer non-recourse loans to safeguard their personal assets, even though these may come with higher rates or stricter terms.

Types of Commercial Loans

There are several financing options available for commercial real estate, each with its own advantages and considerations for property owners:

- Traditional Bank Loans: Offered by commercial banks, these loans typically provide competitive rates but require extensive documentation and a strong credit history.

- SBA Loans: The U.S. Small Business Administration offers 7(a) and 504 loan programs that are ideal for owner-operators seeking favorable terms, lower down payments, and longer repayment periods.

- Bridge Loans: Designed for short-term financing needs, bridge loans help owners quickly secure capital while waiting for long-term financing or during property repositioning. They offer flexibility but often come with higher interest rates.

- Commercial Mortgage-Backed Securities (CMBS): These loans are pooled together and sold as securities to investors. They often feature competitive rates but involve a more complex underwriting process.

- Construction Loans: Tailored for property development, these loans cover the costs of building new properties or renovating existing ones. They typically convert to permanent financing upon project completion.

- Mezzanine Financing: A hybrid between debt and equity financing, mezzanine loans fill the gap between senior debt and the owner’s equity. They can provide additional capital without diluting ownership, though often at a higher cost.

Each loan type has its own set of trade-offs, so understanding your long-term goals and the specific needs of your property is crucial when choosing the right financing option.

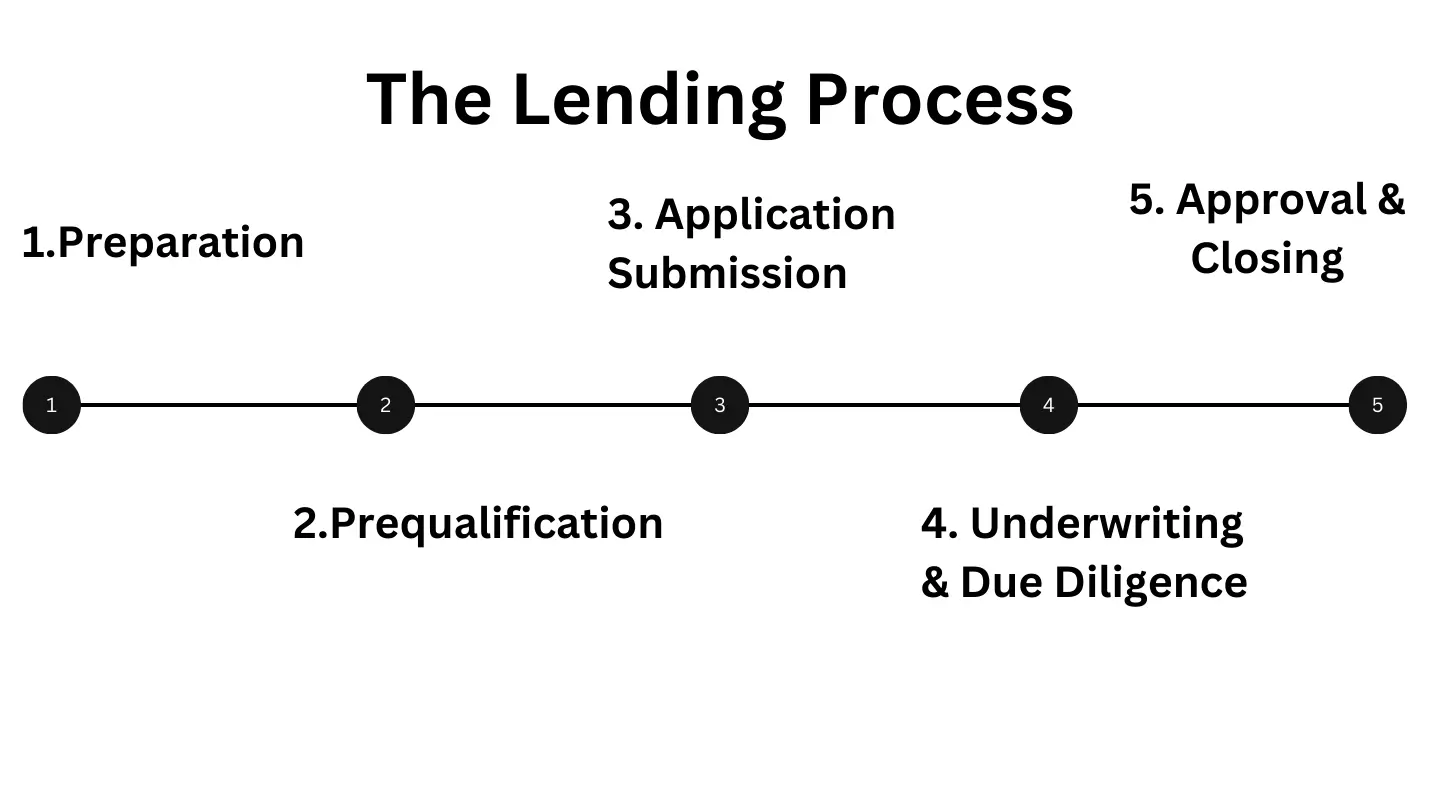

The Lending Process

The journey to secure a commercial real estate loan involves several critical steps. Being well-prepared at each stage can improve your chances of receiving favorable terms:

- Preparation: Assemble comprehensive documentation, including financial statements, property appraisals, rent rolls, occupancy rates, and business plans. For owners, detailed historical data and future projections are essential in demonstrating the property’s potential.

- Prequalification: Many lenders offer a prequalification phase to assess your financial health and the viability of the property. This early step can highlight areas that may need improvement before a full application is submitted.

- Application Submission: Submit your loan application with all required documentation. Be thorough, as incomplete submissions can delay the process.

- Underwriting & Due Diligence: Lenders perform an in-depth review of your creditworthiness, property valuation, market conditions, and overall risk profile. Expect site visits, third-party evaluations, and detailed financial analysis during this stage. Owners may benefit from consulting with financial advisors to ensure all data is presented accurately.

- Approval & Closing: Once the loan is approved, final negotiations on terms—including covenants, prepayment penalties, and interest rate structures—occur. Closing involves finalizing documents and disbursing funds. Understanding each detail can help you negotiate terms that best suit your long-term objectives.

Qualifying for a Loan

To secure a commercial real estate loan, property owners must meet specific criteria. Lenders assess both the financial strength of the borrower and the performance potential of the property:

- Creditworthiness: A strong credit history and robust financial statements bolster your application. Lenders will scrutinize your past performance and overall business stability.

- Property Value & Income: Accurate appraisals and detailed analyses of the property's income-generating capabilities are critical. Demonstrating consistent occupancy and quality tenant profiles can enhance your eligibility.

- Debt Service Coverage Ratio (DSCR): A DSCR greater than 1.2 indicates that the property’s net operating income comfortably covers debt obligations, providing lenders with assurance of the property’s financial resilience.

- Down Payment & Collateral: Adequate equity in the property or additional collateral strengthens your loan application, potentially leading to better terms and interest rates.

By proactively addressing these factors, commercial real estate owners can not only improve their chances of approval but also negotiate more favorable loan terms.

Risk Management

Mitigating risk is essential for protecting your investment and ensuring long-term success. Commercial property owners should consider several risk factors:

- Interest Rate Risk: Fluctuating interest rates can impact monthly payments and overall financing costs. Consider fixed-rate loans or interest rate caps to maintain stability. It is always a good idea to monitor key metrics that impact financing such as the 10 yr treasury yield.

- Market Risk: Economic downturns and local market fluctuations can affect property values and occupancy rates. Stay informed about market conditions and be prepared to adjust your strategy.

- Property-Specific Risk: Factors such as location, tenant quality, and property condition play a crucial role in long-term performance. Regular maintenance and strategic tenant management can mitigate these risks.

- Operational Risk: Unforeseen events such as high tenant turnover or unexpected maintenance issues can disrupt cash flow. Partnering with experienced property management professionals can help maintain consistent operations. To further enhance operational efficiency, check out our Online Rent Collection: The Ultimate Guide for Landlords

- Mitigation Strategies: Diversification of your property portfolio, comprehensive insurance coverage, and regular financial reviews are key strategies to manage and mitigate risks.

Market Trends

The commercial real estate lending landscape is evolving rapidly. As an owner or prospective investor, staying current with these trends can provide a competitive edge:

- Digital Transformation: Lenders are increasingly leveraging digital platforms to streamline application processes, underwriting, and asset management. This results in faster decision-making and greater transparency. To learn more about how technology is revolutionizing property management, explore our The 10 Best Property Management Software For 2025 article.

- Regulatory Changes: New policies and regulations can affect lending criteria, interest rates, and overall market conditions. Regularly review industry updates to stay ahead of these shifts.

- Sustainability & Green Financing: There is a growing emphasis on financing environmentally sustainable projects. Upgrading properties for energy efficiency not only reduces operational costs but can also attract a new segment of eco-conscious tenants.

- Market Volatility: Global economic uncertainties necessitate a more conservative approach to underwriting. Owners who monitor local economic indicators and demographic shifts are better positioned to time refinancing or property acquisitions.

Final Thoughts

For commercial real estate owners and those aspiring to enter the market, a deep understanding of the lending landscape is essential. By familiarizing yourself with key lending terms, the variety of financing options available, and the detailed steps of the lending process, you can secure the capital necessary to grow and sustain your property portfolio.

Effective risk management, proactive preparation, and an awareness of current market trends will further empower you to negotiate favorable terms and build long-term value. Every lending scenario is unique, so it is advisable to consult with financial experts and advisors to craft a financing strategy that aligns with your specific goals.